The Exit and the Entry: SWIFT's CIO Steps Down as Ripple Treasury Joins the Network

The SWIFT exec who called XRP a "fax machine" stepped down on the exact day Ripple walked into SWIFT's partner program. Coincidence or signal? We trace the full story — the feuds, the facts, and what it means for the future of global payments.

The timing is almost too clean to ignore. On the same day Ripple Treasury was confirmed as a SWIFT Certified Partner, the man who spent months publicly mocking Ripple and XRP from inside SWIFT's leadership quietly posted three sentences on LinkedIn and walked out the door.

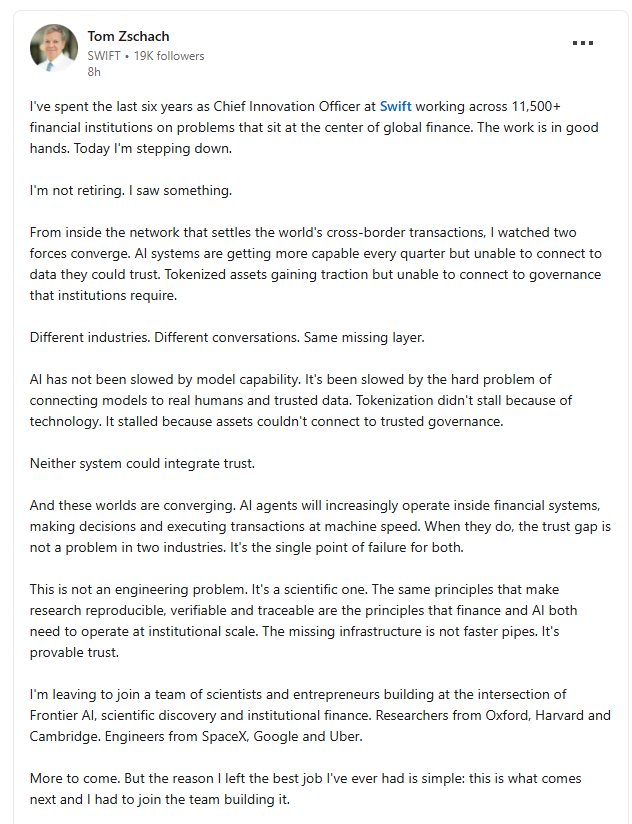

Tom Zschach, SWIFT's Chief Innovation Officer since January 2020, announced his departure on April 2, 2026, writing on his verified LinkedIn profile:

"I've spent the last six years as Chief Innovation Officer at Swift working across 11,500+ financial institutions on problems that sit at the center of global finance. The work is in good hands. Today I'm stepping down."

No elaboration. No named successor. No statement from SWIFT.

Whether these two events are connected is, for now, entirely unconfirmed. But the backdrop of their collision makes this one of the more cinematically satisfying moments the XRP community has witnessed — and it's worth understanding exactly how we got here.

A Documented History of Friction

Zschach's skepticism toward Ripple and XRP wasn't a one-time comment — it was a sustained and escalating public position spanning multiple platforms over more than a year.

The flashpoints began building through mid-2025. When a Ripple supporter praised XRP for surviving its years-long SEC lawsuit, Zschach fired back on LinkedIn:

"Surviving a lawsuit isn't resilience. Neutral, shared governance is. Institutions don't want to live on a competitor's rails."

He doubled down, writing that "compliance isn't about one company convincing regulators it should be allowed to operate — it's about an entire industry agreeing on shared standards that no single balance sheet controls."

The "fax machine" comment came next. Zschach compared using a private token as a "bridge currency" to calling a fax machine "the internet" — a remark widely read as a direct jab at XRP, sparking significant backlash from the Ripple community.

Then came perhaps his sharpest critique. In a separate LinkedIn post, Zschach stated:

"The harder question is whether banks will ever be comfortable outsourcing settlement finality to a token that isn't a deposit, isn't regulated money and doesn't sit on their balance sheet. Liquidity is one thing; legal enforceability is another."

He added that as tokenized deposits and regulated stablecoins scale, banks may see little reason to pay a "toll" to an external asset like XRP when they can settle in instruments they already issue and trust.

He framed his broader philosophy around a simple axiom:

"Every major shift in finance begins the same way. Technology lays the foundation, but trust decides when the building opens."

He called public blockchains "the base environment for execution" — powerful for settlement, but insufficient without legal enforceability, compliance, and privacy. Without that layer, he warned, a public chain is "a fast engine with no cockpit."

Zschach also raised the issue of centralization in the XRP ecosystem directly, suggesting that most institutions won't want to use the XRP Ledger since Ripple is a direct competitor to them, noting that Ripple had applied for a national banking license, which, if approved, would put it in the same league as the banks it aimed to onboard.

It is worth noting: Zschach was not entirely wrong on the technical merits. His critiques echoed legitimate institutional concerns... concerns that Ripple itself has spent years working to address. But the tone was adversarial, the platform was public, and the timing of his departure has now given those comments a very different kind of afterlife.

The Timing Speculation: What Can and Cannot Be Said

The XRP community's reaction on April 2 was immediate and loud, with X posts drawing direct lines between Zschach's exit and Ripple's entry into the SWIFT partner ecosystem.

What is confirmed:

- Tom Zschach announced his own departure in a self-posted LinkedIn statement dated April 2, 2026 — the same day Ripple Treasury's SWIFT Certified Partner listing circulated widely

- Ripple Treasury's confirmed partner status reflects an integration that predates Ripple, going back to GTreasury's Alliance Lite2 connection established around 2014

- No SWIFT press release, named successor, or official explanation for Zschach's departure has been published as of this writing

What is speculation: The causal narrative — that Zschach left because Ripple entered, or was pushed out as SWIFT's strategy pivoted. It is a compelling story, and it may yet prove directionally accurate when/if more facts emerge. But right now, it is community inference, not confirmed reporting.

What can be said without overreach is this: the optics are extraordinary. A senior SWIFT executive who was among the most vocal institutional critics of XRP's fitness for banking infrastructure departed on the exact day Ripple's treasury platform was confirmed as part of SWIFT's certified ecosystem. Readers can draw their own conclusions about what that symbolizes — even if causation remains unproven.

What XRP and SWIFT Actually Are — and Aren't

To understand what all of this means, it helps to clear up a fundamental structural confusion that drives most of the "XRP vs. SWIFT" debate.

SWIFT is not a settlement system — it is a messaging protocol connecting over 11,500 banks worldwide that handles over $5 trillion in daily payment instructions. SWIFT doesn't actually move money; it sends payment orders. The actual funds are shuffled between banks using nostro/vostro accounts, which tie up an estimated $27 trillion in parked liquidity before a transaction is settled.

Ripple's vision is to replace or complement this system using XRP as a bridge asset. Instead of banks holding foreign currencies in multiple countries, they could hold XRP to facilitate real-time currency conversion and settlement — reducing the need for capital-intensive pre-funding and freeing up liquidity. If a U.S. business wants to pay a supplier in Thailand, dollars are converted into XRP, sent across the globe in seconds, and converted into Thai baht on the receiving end.

On raw technical metrics, the comparison is stark. Traditional SWIFT transactions can take one to five business days to settle, depending on the number of intermediaries involved, with fees ranging from $10 to $50 per transaction plus foreign exchange costs. XRP transactions settle in approximately three to five seconds at a cost of fractions of a cent, using On-Demand Liquidity to source capital in real time rather than requiring pre-funded accounts.

The Three Scenarios: Complement, Compete, or Replace

Scenario 1 — XRP as a DeFi Lane Within SWIFT's Infrastructure

This is the scenario Ripple Treasury's SWIFT partnership makes most plausible right now. Rather than replacing SWIFT, XRP operates as a high-speed liquidity lane alongside it. Corporations using Ripple Treasury can choose between traditional SWIFT messaging rails and Ripple's blockchain settlement — giving institutions a parallel, faster track without forcing them to abandon existing infrastructure.

Ripple acknowledges that no single ledger will dominate globally and that interoperability is key. On July 14, 2025, the U.S. Federal Reserve's Fedwire Funds Service officially transitioned to the ISO 20022 messaging format — a major upgrade that analysts believe benefits assets like XRP, already built for ISO 20022 compliance, by making integration with banking networks smoother.

SWIFT's new retail payments framework already covers 50-plus banks and 25-plus corridors going live by mid-2026, and at least 30 of those banks already have ties to Ripple's ecosystem — making the overlap between the two systems increasingly significant.

Scenario 2 — Competitive Displacement Over Time

Ripple's Navin Gupta has described the firm's approach as "zero or one" — either fundamentally changing how value moves across borders or fading away. Ripple CEO Brad Garlinghouse has publicly targeted capturing 14% of SWIFT's transaction volume within several years, though some analysts argue even that figure is conservative given the network effects of full institutional adoption.

A full replacement is unlikely in the near term — XRP is more realistically positioned to complement SWIFT by capturing a share of lower-value, high-frequency cross-border payment corridors. Garlinghouse has stated that Ripple's goal is specifically to replace SWIFT's liquidity layer, not the entire messaging architecture — a narrower but still enormously consequential ambition.

Scenario 3 — The Institutional DeFi Layer

Perhaps the most forward-looking scenario is XRP's evolving role in institutional DeFi — not as a consumer crypto asset but as programmable settlement infrastructure for tokenized assets.

By leveraging the XRP Ledger, Ripple streamlines post-trade processes and enables 24/7 instant settlements, accelerating the convergence of traditional finance and blockchain technology. RippleNet had expanded to over 300 institutions by December 2025, with XRP's role in DeFi beginning to take shape through tools like Digital Asset Accounts and the Unified Treasury interface.

XRP network usage jumped approximately 38% year over year in 2025, driven by DeFi activity, tokenized assets, and rising institutional payment flows. The XRPL has recorded daily peaks above 5.1 million transactions while maintaining near-100% success rate and low fees. Ripple now holds full or expanded licenses in ten-plus key jurisdictions, including Singapore's MAS regime.

The Barriers That Remain Real

Zschach's critiques, however sharp, were not entirely without substance. The honest analysis requires acknowledging what still stands in the way.

Institutional players won't move serious volume until there's clear, coordinated global regulation. Replacing SWIFT would also threaten entrenched interests, jobs, and national infrastructures — resistance from major banks and regulators invested in maintaining control over the status quo should be expected. Nations may also resist any neutral cross-border solution they don't directly influence, and there is no global consensus in the short term, even if the technology is ready.

Most RippleNet-connected banks still use RippleNet for messaging only — around 40% use On-Demand Liquidity, which is the product that actually requires XRP as a bridge asset. For the token to benefit materially, institutions need to shift from messaging-only to ODL. That shift depends on whether the cost savings of using XRP as a bridge asset outweigh the compliance burden of holding a digital asset on their balance sheets.

Price volatility, hardware custody risk, and the political sensitivity of cross-border monetary infrastructure all remain live concerns. SWIFT's own blockchain initiatives — particularly its work with Chainlink's CCIP for tokenized asset transfers — show that traditional finance is not sitting still.

Bottom Line

Tom Zschach spent the better part of a year telling anyone who would listen that XRP was a fax machine, that public chains were engines without cockpits, and that banks would never trust Ripple's rails. Then he stepped down — on the day Ripple's treasury platform was confirmed as a certified partner inside the very network he helped run.

Whether that is poetic justice, coincidence, or something more deliberate may become clearer in the days ahead. What is already clear is that the boundaries between Ripple and SWIFT are dissolving faster than Zschach's public commentary ever acknowledged — and that the most honest version of the XRP-SWIFT story is not "replacement vs. coexistence" but rather a gradual integration that makes the original rivalry increasingly hard to define.

DISCLAIMER: This newsletter is for informational purposes only and does not constitute investment advice, advertising, or a recommendation to buy, sell, or hold any securities. This content is not sponsored by or affiliated with any of the mentioned entities. Investments in cryptocurrencies or other financial assets carry significant risks, including the potential for total loss, extreme volatility, and regulatory uncertainty. Past performance is not indicative of future results. Always consult a qualified financial professional and conduct thorough research before making any investment decisions.

Sources

| # | Source | Description |

|---|---|---|

| 1 | Tom Zschach – LinkedIn Profile | Primary source for his April 2, 2026 departure announcement |

| 2 | Ripple Treasury – Connectivity Partners | Official SWIFT Certified Partner confirmation |

| 3 | DailyCoin – SWIFT Honcho Roasts Ripple's Legal Grind | Documents Zschach's "surviving a lawsuit" LinkedIn comments, September 2025 |

| 4 | Bitcoinist – Banks Won't Trust Ripple and XRP, SWIFT CIO Says | In-depth coverage of Zschach's trust and governance arguments |

| 5 | Yahoo Finance / CryptoSlate – SWIFT CIO Questions Ripple and XRP's Readiness | Zschach's settlement finality challenge and "fast engine, no cockpit" quote |

| 6 | Bitcoinist – Ripple vs. SWIFT Battle Heats Up with "Fax Machine" Comment | Documents the "fax machine vs. internet" controversy, October 2025 |

| 7 | Financial Planning Association – How Ripple is Building a Bridge to Cross-Border Transactions | Authoritative structural analysis of SWIFT's nostro/vostro inefficiencies vs. XRP's ODL model |

| 8 | 24/7 Wall St. – SWIFT Names 30 Ripple-Connected Banks | SWIFT's new retail payments framework and Ripple's institutional overlap |

| 9 | CoinDCX – Ripple Bridges XRP Into SWIFT Network Through ILP | ISO 20022 alignment and Federal Reserve Fedwire transition context |

| 10 | MEXC Learn – Will XRP Replace SWIFT? | Balanced analysis of replacement vs. complement scenarios |

| 11 | CoinLaw – XRP vs. SWIFT Statistics 2026 | Transaction speed, fees, and adoption metrics comparison |

| 12 | DailyCoin – XRP Analyst Argues Ripple Aims to Replace SWIFT, Not Complement | Ripple executive "zero or one" quote and network effect analysis |

| 13 | Ainvest – XRP Poised to Disrupt SWIFT in 2026 | Garlinghouse's 14% SWIFT volume target and institutional adoption roadmap |