Ripple's Fingerprints Are All Over SWIFT's New Banking Framework

SWIFT just named 50+ banks for its June 2026 blockchain payment overhaul — and at least 30 already partner with Ripple. We break down what the overlap actually means for XRP, and what it doesn't.

SWIFT just named 50+ banks for its blockchain-powered payments overhaul launching June 2026 — and at least 30 of them already have ties to Ripple. Here's what that actually means.

What SWIFT Has Announced

SWIFT officially confirmed on March 5, 2026 that more than 25 banks have committed to processing payments under its new cross-border payments framework by June, covering corridors across Australia, Bangladesh, Canada, China, Germany, India, Pakistan, Spain, Thailand, the UK, and the US.

The new payments framework is one half of SWIFT's broader innovation strategy — the other being a blockchain-based shared ledger joining SWIFT's infrastructure stack. The framework is designed to speed cross-border payments for consumers and small businesses, extending its advantages to 4 billion accounts across more than 200 countries and territories.

The framework targets a core inefficiency: up to 80% of a payment's total processing time is consumed in the "last mile" — the gap between funds arriving at a receiving bank and final delivery to the customer. SWIFT's system promises upfront fee certainty, full-value delivery without intermediary deductions, near-instant settlement where local infrastructure allows, and end-to-end traceability on every transaction.

The blockchain-based shared ledger component focuses on enabling 24/7, real-time cross-border payments and the trusted, scalable movement of regulated, tokenized value across SWIFT's network of 11,500 financial institutions spanning more than 200 countries.

The Ripple Overlap Nobody Can Ignore

What caught the crypto community's attention was the participant list. At least 30 of the 50+ banks SWIFT named already have ties to Ripple, including Santander, HSBC, Deutsche Bank, Standard Chartered, and JPMorgan. SWIFT didn't mention Ripple once in the announcement, but the overlap between its new framework and Ripple's existing bank network sparked immediate curiosity among XRP investors.

The connections run deep across multiple regions:

- Akbank was among the first adopters of Ripple-based blockchain payments in Turkey. ANZ Bank tested the protocol as early as 2015. Axis Bank has operated active RippleNet corridors in India since 2017, and Bank Alfalah has used Ripple's infrastructure for UAE–Pakistan remittances since 2021.

- Santander powers its One Pay FX international transfers through RippleNet. Deutsche Bank combined Ripple's blockchain infrastructure with SWIFT earlier in 2026 to build an enhanced cross-border payment ledger. Major banks like HSBC, Standard Chartered, Bank of America, and JPMorgan have all piloted or integrated Ripple's technology in some form.

- In Asia, Japan's SBI Remit and Thailand's Siam Commercial Bank have live XRP liquidity corridors. RippleNet customers also include banks in Pakistan (Faysal Bank), Qatar, and Bangladesh (bKash), as well as fintechs like Finastra in the UK.

What's important is that these banks are now operating inside both ecosystems simultaneously — building with SWIFT's new framework while maintaining their existing Ripple connections. They're not choosing one over the other, and that says a lot about where cross-border payments are heading.

The Thunes Bridge: SWIFT, Ripple, and XRP's Hidden Connection

Beyond the direct bank overlap, there's a structural connection that is more subtle — and potentially more significant.

SWIFT's blockchain push positions XRP as an optional liquidity rail inside the network. The mechanism runs through Thunes, a payments company now embedded in SWIFT's network, whose connections reach Ripple's payment products and, by extension, XRP's On-Demand Liquidity functions. The routing sequence: a company sends a payment via SWIFT; SWIFT routes through Thunes; Thunes offers access to Ripple's ODL infrastructure; XRP settles the leg. No step in that chain forces a bank to use XRP — the optionality is built in, not mandated.

SWIFT ran a successful trial with Citi using USDC in November 2025 and completed a proof-of-concept with HSBC and Ant International for tokenized deposit transfers the following month. A January 2026 trial with BNP Paribas Securities Services, Intesa Sanpaolo, and Societe Generale FORGE settled tokenized bonds against fiat and digital payments. The institution is stress-testing every digital asset rail available — and XRP's rail is now wired in.

XRP / Ripple Analysis: What This Means (And What It Doesn't)

This is where clear heads matter more than excited headlines.

What's Confirmed: Ripple has built an extensive partner network that overlaps heavily with SWIFT's new framework participants. RippleNet now counts over 300 banks and financial institutions across six continents as clients.

What's Not Confirmed — And Critically Important:

The Ripple solution most banks use is RippleNet, and it doesn't automatically mean using XRP. RippleNet is a messaging and settlement network that banks can run entirely in fiat. Only around 40% of RippleNet partners use Ripple's On-Demand Liquidity service — the product that actually requires XRP as a bridge asset between currencies.

SWIFT's new framework is a win for Ripple's credibility but not yet a win for XRP. The 30-bank overlap proves that Ripple has built its infrastructure in the right places. The same corridors and institutions that SWIFT considers essential to the future of cross-border payments are all tied to Ripple. But most of those banks use RippleNet for messaging without touching XRP, and SWIFT's framework doesn't require XRP at any point in the payment flow.

The Stablecoin Competitor:

Stablecoins offer many of the advantages of XRP — speed, cost, and built-in recordkeeping — without the volatility. A bank takes on significant risk by holding any portion of XRP, since the token can lose 10% of its value rapidly. Stablecoins don't fluctuate meaningfully in price, making them closer to true digital cash, and major banks are watching them closely.

The Key Variable to Watch:

For the token to benefit, banks already on RippleNet need to start shifting from messaging-only to On-Demand Liquidity. That dynamic depends on whether the cost savings of using XRP as a bridge asset outweigh the compliance burden of holding a digital asset on their balance sheets. The trigger worth watching is mid-2026, when the first wave of SWIFT corridors goes live. If banks in the India-Pakistan, UAE, and Southeast Asian corridors start routing payments through Thunes into Ripple's ODL rails — because it's faster and cheaper than what SWIFT's own framework delivers — that's when real demand for XRP could show up in the price.

What the Community Is Saying

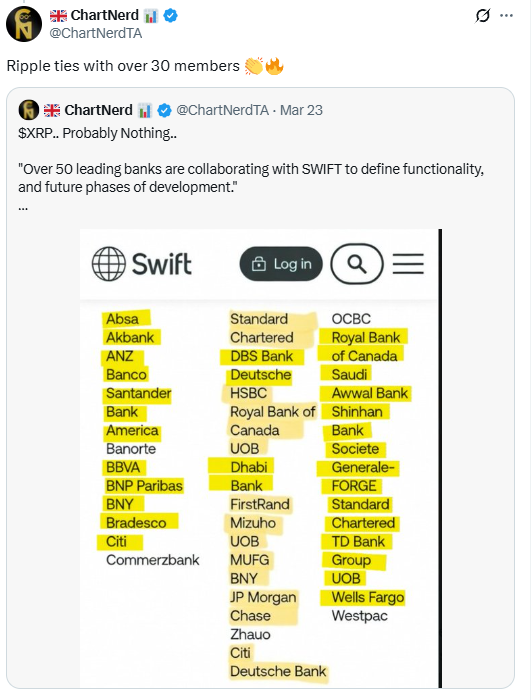

ChartNerd (@ChartNerdTA), a widely followed technical analyst on X, highlighted the overlap on April 2, 2026, noting "Ripple ties with over 30 members" while annotating the SWIFT bank list with Ripple-connected institutions. Chad Steingraber (@ChadSteingraber) added in his LAW DAY 256 post that SWIFT stated "each bank will use its own interoperable system of choice," and that "a lot of these are Ripple partners." These are community observations — not official statements from Ripple or SWIFT.

Key Takeaways

The SWIFT-Ripple story in 2026 is genuinely significant, but it requires careful framing. SWIFT has launched its most ambitious payments overhaul in history, with 50+ global banks signed on and a blockchain layer being woven into its infrastructure. The fact that roughly 30 of those banks already have RippleNet relationships is not a coincidence; Ripple spent years building in precisely the corridors that global regulators and institutions now consider highest priority.

But the distance between "Ripple partners are in SWIFT's framework" and "XRP will benefit from it" is real and should not be glossed over. Banks operating in both ecosystems dosen't necessarily mean they're using XRP. The mid-2026 corridor launches will be the first genuine test of whether ODL adoption accelerates, or whether banks continue routing payments through messaging-only RippleNet rails — or SWIFT's own blockchain infrastructure — without touching XRP at all.

The infrastructure is in place. The partnerships exist. Whether the token itself benefits depends on choices that banks haven't publicly committed to yet.

DISCLAIMER: This newsletter is for informational purposes only and does not constitute investment advice, advertising, or a recommendation to buy, sell, or hold any securities. This content is not sponsored by or affiliated with any of the mentioned entities. Investments in cryptocurrencies or other financial assets carry significant risks, including the potential for total loss, extreme volatility, and regulatory uncertainty. Past performance is not indicative of future results. Always consult a qualified financial professional and conduct thorough research before making any investment decisions.